Process Type

Graphical expression

Mind Type

Structured expression

Note Type

Efficient expression

Treemap

Bracket Diagram

Default Mode

Many companies fail in financing, IPOs, or even internal power struggles among founders because of a poorly designed equity structure. It's not just a formality for business registration; it's the underlying code for power distribution, interest dynamics, and strategic direction within the company.

This article will systematically explain what an equity structure diagram is, common types of corporate equity structures, and how to use professional tools (such as ProcessOn) to draw a clear and compliant equity structure diagram, helping entrepreneurs, managers, HR professionals, and investors quickly understand corporate governance structures.

A shareholding structure diagram is a graphical representation of a company's shareholders, their shareholding percentages, investment relationships, control levels, and the relationships between these entities. It answers three core questions:

Who are the company's shareholders? (Individuals, legal entities, partnerships, funds, etc.)

What percentage? What is the shareholding percentage of each shareholder?

How to control it? Through special arrangements such as concerted action agreements between shareholders, proxy voting, and dual-class shares.

Simply put, a shareholding structure diagram is a company's "ownership map." Through this diagram, you can see at a glance: Who is the actual controller? Is there an absolute controlling shareholder? How is the employee stock ownership platform set up? What is the weight of external investment institutions?

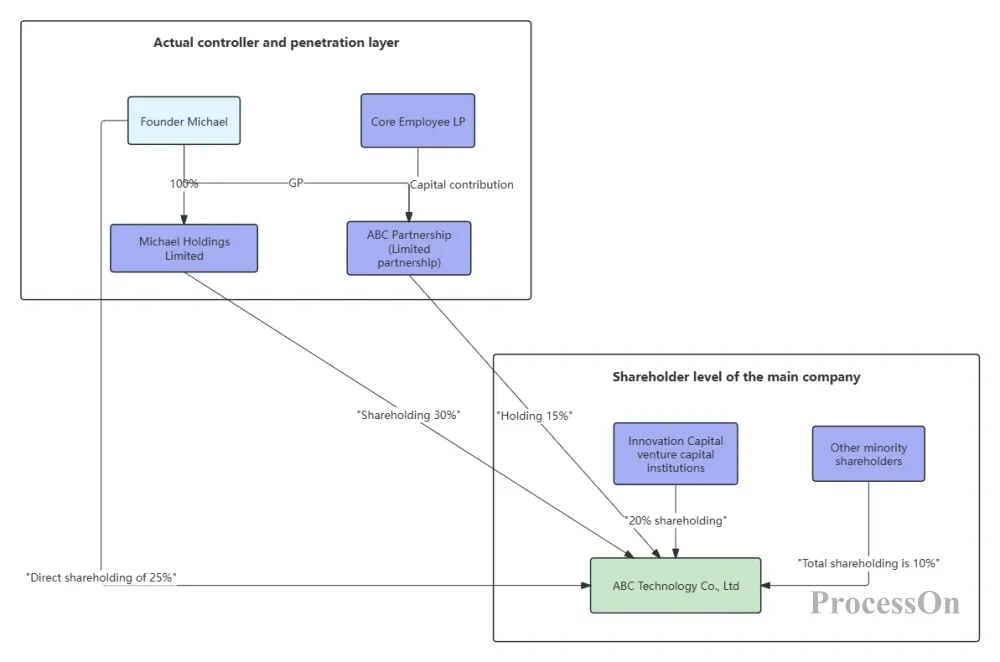

Equity Structure Diagram of Technology Co., Ltd.

Clearly define rights and responsibilities: Clearly define the boundaries of power for shareholders, directors, supervisors, and senior executives to avoid internal disputes.

Assisted financing: Investors can quickly assess a company's governance structure and determine investment risks by using its organizational chart.

Tax planning: The tax burden varies greatly depending on the shareholding method (direct shareholding by natural persons vs. shareholding by holding companies vs. limited partnerships).

Control structure: Control the company with a small number of shares through multi-layered structures, dual-class shares, concerted action agreements, etc.

Compliance requirements: IPOs and listed companies must provide a complete equity structure diagram in their information disclosure.

Based on the company's development stage, shareholder identities, and tax considerations, equity structures can be summarized into the following classic models:

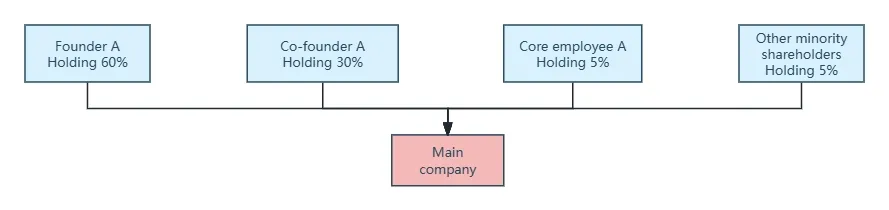

Structure: Founders, co-founders, core employees, and other natural persons all directly hold shares in the company.

Features:

Simple and intuitive, with clear business registration information.

Tax burden: 20% personal income tax is payable when dividends are distributed; 20% property transfer income tax is payable when equity is transferred.

Suitable for: startups, closed companies, and companies with a small number of shareholders and simple relationships.

Disadvantages: Poor risk isolation (shareholders' personal debts may affect the company), limited room for tax planning.

Direct shareholding structure by natural persons

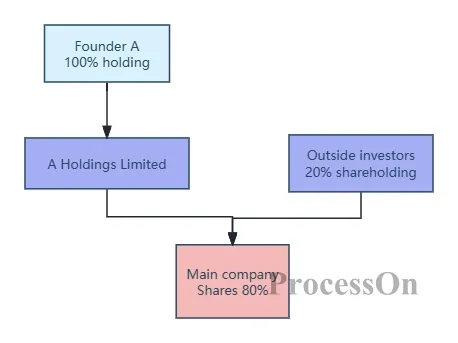

Structure: The founder first establishes a holding company (usually a limited liability company), and then the holding company holds the equity of the main company.

Features:

A holding company can act as a "money bag," aggregating the profits from its various business segments.

Tax advantages: Dividends received by the holding company from the parent company are tax-exempt (between resident enterprises), and no tax needs to be paid when reinvesting.

Risk isolation: An extra layer of firewall is added between individuals and business operations.

Suitable for: diversified conglomerates and entrepreneurs who plan to hold multiple business segments for the long term.

Disadvantages: An additional layer of company means an additional layer of maintenance costs (bookkeeping, tax filing, annual inspection).

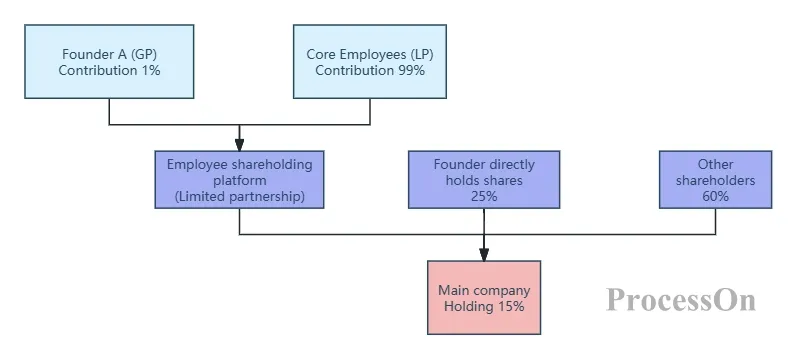

Structure: The founder acts as the general partner (GP), and the employees or investors act as limited partners (LP) to jointly establish a limited partnership, which then holds shares in the main company.

Features:

Separation of power and money: GP (usually contributing very little capital) has all decision-making power; LP (actual investors) only enjoy the right to profit and do not participate in management.

Tax look-through: Limited partnerships do not pay income tax themselves; instead, taxes are paid directly at the level of the partners.

Ideal for: Employee stock ownership plans (employees as limited partners (LPs) and founders as general partners (GPs), avoiding the dispersion of decision-making due to direct employee shareholding); private equity funds.

Common usage: Many listed companies have set up "employee stock ownership platforms" (limited partnerships), where the founder controls the general partner (GP) and firmly holds the voting rights.

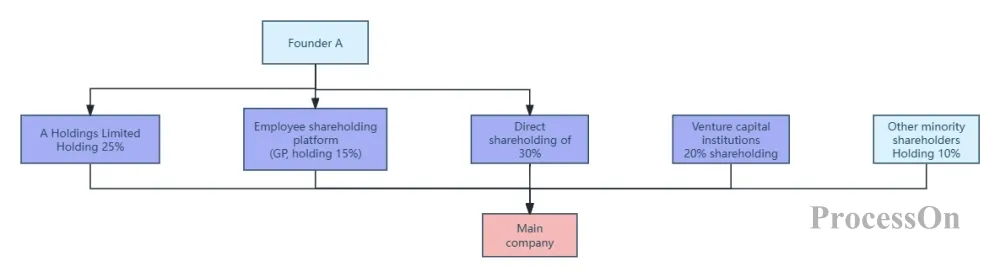

Structure: Combining various forms such as individual shareholding, holding companies, and limited partnerships. For example, the founder directly holds a portion of the shares, while also holding another portion through a holding company, and an employee shareholding platform is also established.

Features: Flexible, allowing for the adoption of the optimal shareholding method based on the nature of different shareholders (founders, financial investors, employees).

Founder: Direct shareholding + holding company (to facilitate the cashing out of some equity while retaining control).

External investors: They usually hold shares directly, which makes it easier to exit.

Employees: Shareholding through limited partnerships avoids the dispersion of voting rights.

Suitable for: Mature companies that have completed multiple rounds of financing and are preparing for an IPO.

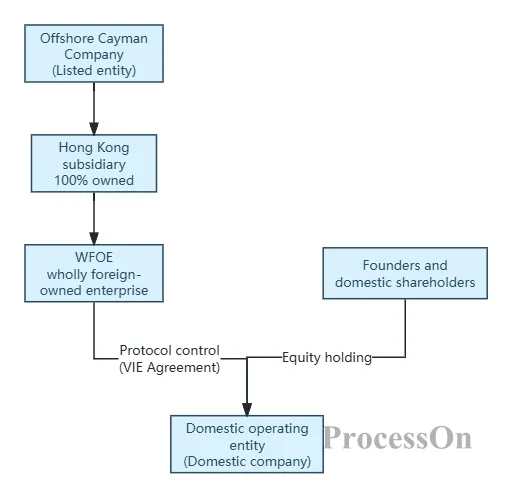

Structure: The domestic entity and the overseas listed company are controlled through a series of agreements (rather than equity control), mainly used to circumvent foreign investment restrictions in industries such as the Internet and education.

Characteristics: Complex, involving Cayman Islands companies, Hong Kong companies, WFOEs (Wholly Foreign-Owned Enterprises), and domestic operating entities. Typically, the offshore Cayman Islands company serves as the listing entity, effectively controlling the domestic company through layers of agreements.

Suitable for: Internet, education, media and other foreign-invested restricted industries that plan to list overseas (US stock, Hong Kong stock).

VIE architecture ( simplified illustration )

Drawing a shareholding structure diagram doesn't require a complex financial background; the key is to clarify the shareholding hierarchy and control relationships. Here are the standard steps:

List all direct shareholders (individuals, companies, partnerships, etc.).

For each corporate shareholder, continue tracing upwards until the final natural person or state-owned asset supervision and management agency.

Record the shareholding ratio, subscribed capital, and paid-in capital of each entity.

Equity structure diagrams typically use a tree structure, showing control relationships from top to bottom (or from left to right).

Root node: Actual controller (ultimate shareholder).

Intermediate nodes: holding company, limited partnership, employee stock ownership platform.

Leaf node: Main company (operating entity).

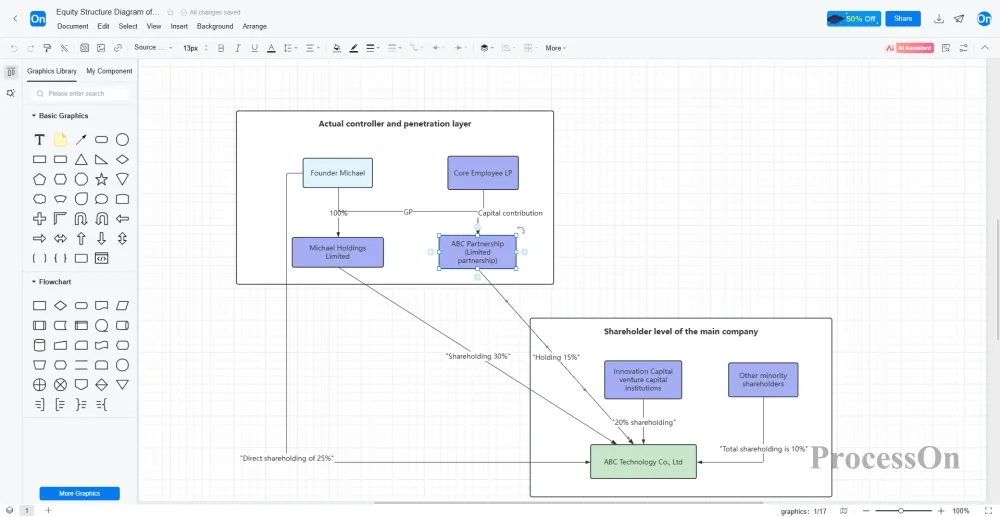

We recommend using the ProcessOn online flowchart tool:

It has multiple built-in templates; you can find ready-made examples by searching for "equity structure" or "equity structure".

It supports free dragging and automatic alignment, making it easy to draw multi-level holding relationships.

You can add icons and colors to distinguish different types of entities (blue for individuals, green for companies, and orange for partnerships).

It supports team collaboration, making it easy for legal, financial, and founder teams to edit together.

Export to multiple formats such as PNG, PDF, and Visio, which can be directly used for financing business plans or business registration.

Create a new flowchart, or use the "Equity Structure Diagram" template.

Place the "Main Company" rectangle in the center of the canvas.

Add a shareholder layer above: Draw the shareholders who hold direct shares (such as founders, employee stock ownership platforms, and investment funds).

Continue to trace upwards: If the shareholder itself is a holding company or partnership, continue to draw out its partners or parent company.

Labeling information: Next to each node, label the shareholding ratio, capital contribution, and voting rights ratio in small print (if different from the shareholding ratio).

Add relationship lines: Use solid lines with arrows to represent shareholding relationships, and you can mark the percentages on the lines.

If there is a concerted action agreement or special voting rights arrangement, it can be indicated with a dashed box or a note.

Use colors and legends: for example, green represents "shareholding entities controlled by the actual controller" and red represents "external financial investors".

Ensure that the total shareholding ratio of all levels is 100% (or disclose the remaining "other minority shareholders").

Check for any circular shareholdings or contradictions.

For complex VIE structures, they can be divided into two diagrams: one is the "equity control relationship diagram" and the other is the "contractual control relationship diagram".

Drawing only one layer: Only showing the direct shareholders of the main company without going up to the actual controller makes it difficult to understand the true control chain.

Ignore voting rights differences: If there are A/B shares or concerted action agreements, they must be clearly marked in the diagram, otherwise it will mislead the reader.

Inaccurate proportions: Especially after multiple rounds of financing, the equity ratio may be diluted, and the latest data must be updated.

Graphic clutter: Intersecting lines and cluttered nodes make it difficult to read. Use professional tools for automatic layout or manually tidy it up.

A shareholding structure diagram is like an "X-ray" of corporate governance. Whether you're the founder of a startup or a manager of an established company, you should review and update it regularly. A clear and compliant shareholding structure diagram can not only help you avoid control disputes but also win the trust of investors during fundraising and IPO processes.

Now, open ProcessOn and start by drawing your company's first equity structure diagram. If you're stuck for ideas, you can search for "startup equity structure" or "employee stock ownership platform structure" in the template community to learn from successful examples.

Making equity visible and clearly defining power—that's the greatest value of a good equity structure diagram.